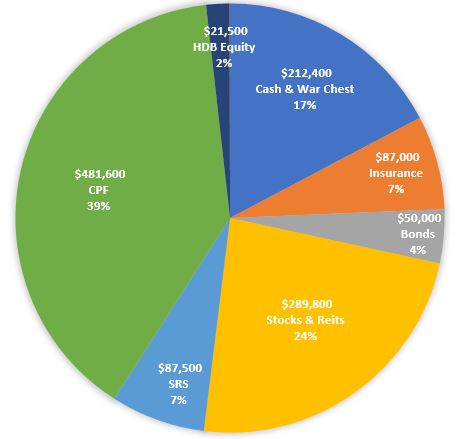

The first quarter of 2022 has come to an end. It is time for me to review my investment portfolios.

The stock markets have rebounded strongly after undergoing several weeks of turbulence with the ongoing war in addition to immense noises engulfing Fed tapering, interest rates hikes, inflation fears, Omicron variant fears, rise of US Treasury yields and so on.

Whether it is the resumption of a bull market or a fake breakout is uncertain. Nevertheless, time in the market always beats timing the market.

I remain invested and plan to slowly and steadily increase my investments in income-producing assets and growth businesses in the coming few weeks, for the long-term.

My SGX Income Portfolio value recovers to $282k from $268k last month mainly due to recovery of Reits.

1. Added 1,000 shares of OCBC at $11.56.

Portfolio Dividends

1. Received $119.50 of dividends from Savings Bonds on 1 Mar.

2. Received $138.08 of dividends from Ascott Reit on 1 Mar.

3. Received $298.14 of dividends from Keppel Reit on 1 Mar in SRS account.

4. Received $92.77 of dividends from Capitaland China Trust on 7 Mar.

5. Received $280.48 of dividends from Keppel DC Reit on 10 Mar in SRS account.

6. Received $759.80 of dividends from Ascendas Reit on 11 Mar.

7. Received $66.60 of dividends from Capitaland Integrated Commercial Trust on 15 Mar.

8. Received $279.20 of scrip dividend as 109 shares from Mapletree Industrial Trust on 15 Mar.

9. Received $72.40 of dividends from Mapletree Logistics Trust on 22 Mar.

10. Received $752 of dividends from Aims Apac Reit on 25 Mar.

SGX Income Portfolio

Moomoo

Tiger Broker

SRS Ultra Long-Term Portfolio

As always, stay safe and remain strong.