Today is the last day of May 2022 for me to review my investment portfolios.

The stock markets have remained volatile engulfed under the immense noises engulfing Fed tapering, interest rates hikes, inflation fears, recession fears, Omicron variant fears, rise of US Treasury yields, Ukraine war, poor company quarterly results and so on.

Whether it will stay as a bear market or merely just a correction remains uncertain. There are emerging signs of stabilization and rebound. Nevertheless, time in the market always beats timing the market. Every market tank leads to a rebound, stronger than ever before.

The stock market always and only goes up, at least for the S&P 500 or Dow Jones. SGX and HSI have no guarantee of such trend though.

I remain invested and continue to hunt for income-producing assets and growth businesses in the coming few weeks, for the long-term.

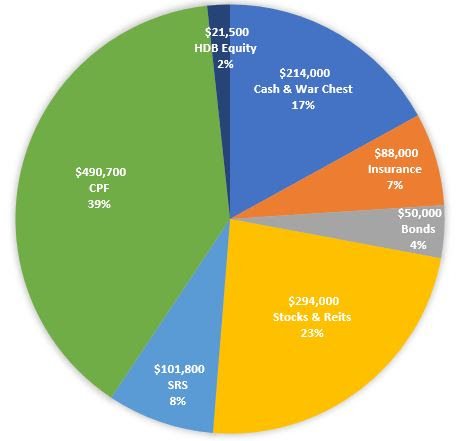

My SGX Income Portfolio value plummets to $271.4k from $283.2k last month mainly due to the rather heavy correction of S-Reits to reflect the impact of interest rate hikes.

1. Assigned 100 shares of Palantir Technology Inc. at $20 from a PLTR220819 put option with $20 strike price on Moomoo.

2. Subscribed $9,000 of Astrea 7 PE Class A-1 bonds successfully. My bonds are not reflected and tracked in SGX Income Portfolio.

Portfolio Dividends

1. Received $114 of dividends from Savings Bonds on 1 May.

2. Received $157.50 of dividends from Wilmar on 6 May in SRS account.

3. Received $72 of dividends from Sembcorp Industries on 10 May.

4. Received $470 of dividends from ST Engineering on 10 May in SRS account.

5. Received $370.20 of dividends from UOB on 13 May.

6. Received $960.12 of dividends from OCBC on 20 May in SRS account.

7. Received $42 of dividends from OUE on 26 May.

8. Received $105 of dividends from Comfortdelgro on 27 May in SRS account.

9. Received $184.08 of dividends from Frasers Centrepoint Trust on 30 May.

10. Received $119.55 of dividends from Suntec Reit on 30 May.

SGX Income Portfolio

Moomoo

Tiger Broker

SRS Ultra Long-Term Portfolio

Thank you for reading. As always, stay safe and remain strong.