1. Parkway Life Reit (SGX: CP2U)

2. Keppel DC Reit (SGX: AJBU)

3. Mapletree Industrial Trust (SGX: ME8U)

4. Mapletree Logistics Trust (SGX: M44U)

5. Ascendas Reit (SGX: A17U)

Let me continue to share on the 6th to 10th Best Reits. I have excluded the likes of hospitality Reits such as Ascott Residence Trust (SGX: HMN) and CDL Hospitality Trust (SGX: J85) as they are heavily impaired by the current coronavirus situation.

6. Mapletree Commercial Trust (SGX: N2IU)

It owns a S$7B portfolio of properties comprising of the following:

i. Vivocity - Singapore's largest mall located in Harbourfront

ii. Mapletree Business City I & II- an integrated office and business park Grade A building complex

iii. PSA Building - an integrated office and commercial made up of a 40 storey office block attached to Alexandra Retail Centre

iv. Mapletree Anson - a 19 storey Grade A office building in Singapore's CBD

v. Bank of America Merill Lynch Harbourfront - a 6 storey premium office building

This Reit is the biggest beneficiary from Singapore's Greater Southern Waterfront (GSW) as 5 of its properties are located in this precinct. The government has announced plans to rejuvenate and inject life in the GSW through developments of private and public housing, office space, recreation and park connectors to make it a great place to live, work and play. More than 2000 hectares of land, 6 times the size of Marina Bay are reserved for future development - Keppel Golf Club, Pasir Panjang Power District, PSA City Port and Pasir Panjang Port Terminals.

There is a clear potential growth pipeline for this Reit as it has the first rights of refusal from its parent and sponsor, Mapletree to the following properties in GSW.

i. Harbourfront Centre

ii. Mapletree Lighthouse

iii. St James Power Station

vi. Mapletree Anson

v. PSA Vista

vi. Harbourfront Tower

vii. Keppel Bay Tower

Since IPO, this Reit has been rewarding shareholders with consistent and increasing DPU. Its steady growth through yield accretive acquisitions are testament of the manager's foresight and pragmatism.

The impact from current pandemic presents a great buying opportunity as its share price plunged to the lows of $1.50s, a level seen more than 3 years ago. At a share price of $1.90, estimating a conservative dividend per share of $0.080 for FY20/21 gives a yield of 4%. Powered by population growth in the GSW, recovery of tourism to Sentosa island and as an STI Component constituent, there is only one certain direction for this Reit. Northward to the skies!

7. CapitaLand Mall Trust (SGX: C38U)

I am forward visualising CapitaLand Mall Trust becoming the combined entity, CapitaLand Integrated Commercial Trust (CICT) even though the merger with CapitaLand Commercial Trust (SGX: ND8U) has not yet completed by Sep 2020. CICT will be the third largest Reit in the Asia Pacific region owning S$22.9B worth of 10 top notch premium commercial properties and 15 shopping malls. With a market capitalisation of more than S$15B, CICT will overtake Ascendas Reit to become the godly Mega Reit in Singapore. By owning CICT, you will enjoy a stake in the following well-diversified basket of properties:

Commercial Properties

1. Capital Tower, a 52-storey Grade A office tower

2. Asia Square Tower 2, a 46-storey Grade A office tower

3. Six Battery Road, a 42-storey Grade A office tower

4. One George Street (50% interest), a 23-storey Grade A office tower

5. Raffles City Singapore (60% interest), an integrated development comprising a 42-storey Raffles City Tower, 5-storey Raffles City Shopping Centre, 73-storey Swissotel the Stamford and 28-storey Fairmont Singapore and a convention centre

6. CapitaGreen, a 40-storey Grade A office tower

7. 21 Collyer Quay, a 21-storey prime office building

8. CapitaSpring (45% interest), an integrated development with an office tower, a serviced residence, ancillary retail and food centre to be completed in 1H 2021

9. Gallileo (94.9% interest), a Grade A commercial building with ancillary retail and a 4-storey heritage building for office use located in Frankfurt, Germany's prime Central Business District

10. Main Airport Center (94.9% interest), a freehold 11-storey multi-tenanted office building in Frankfurt Airport, Germany

Shopping Malls

1. Junction 8

2. IMM Building

3. Bugis Junction

4. Raffles City Singapore (40% interest)

5. Bukit Panjang Plaza

6. Clark Quay

7. Westgate

8. Tampines Mall

9. Funan

10. Plaza Singapura

11. Jcube

12. Lot One Shopping Mall

13. The Atrium@Orchard

14. Bugis+

15. Bedok Mall

On top of all these, you will get some dessert in the form of an 11% stake in CapitaLand Retail China Trust, indirectly owning another 14 malls spread across 9 cities in China.

The benefits of the merger are explained in my post in CMT + CCT = CICT.

Net Property Income and DPU for CapitaLand Mall Trust have increased every year except for 2017 when Funan was closed for redevelopment.

For CapitaLand Commercial Trust, Net Property and Distributable Income rise steadily in the past years through strategic yield accretive acquisitions.

Occupancy rate for the shopping malls is 99.3% as of 31 Dec 2019 but this may be impacted by the current situation whereby smaller businesses may have to close down if they cannot withstand the loss of income during the 2 months of circuit breaker. The commercial properties currently have an occupancy of above 96%. Rental reversion for shopping malls is at 0.9% and is positive for commercial properties in 2019 despite a sluggish economy.

In terms of performance and growth prospects, it will be very challenging for CICT in the short term which could take up to 1 or 2 years. The relief package and rebates for Apr and May 2020 rentals for tenants will make subsequent quarterly results ugly. Drop in Net Property Income, DPU and negative rental reversions are expected. The merger is expected to be completed by 3Q 2020 and I do not expect any acquisition of properties soon because the gearing for CICT after merger will rise up to 39% but still below the stipulated debt ceiling of 45%.

In the mid term of 2 to 5 years, CICT will have a potential pipeline of exciting and high quality acquisitions from its parent and sponsor Capitaland. Singpost Centre, Ion Orchard, The Star Vista, Changi Airport just to name a few in Singapore. And there is no shortage of shopping malls and commercial properties in Asia and across Europe for injection into this combined Reit by Capitaland.

At share price of $1.80, an estimated dividends of $0.09 per share for FY2020 will yield 5%. In FY2023, a projected dividends of $0.125 per share will yield 6.9%. In the long term, there is a dwindling supply of shopping malls and commercial properties in Singapore hence in the next economy recovery phase, I believe CICT will definitely recover in style and soar to greater heights!

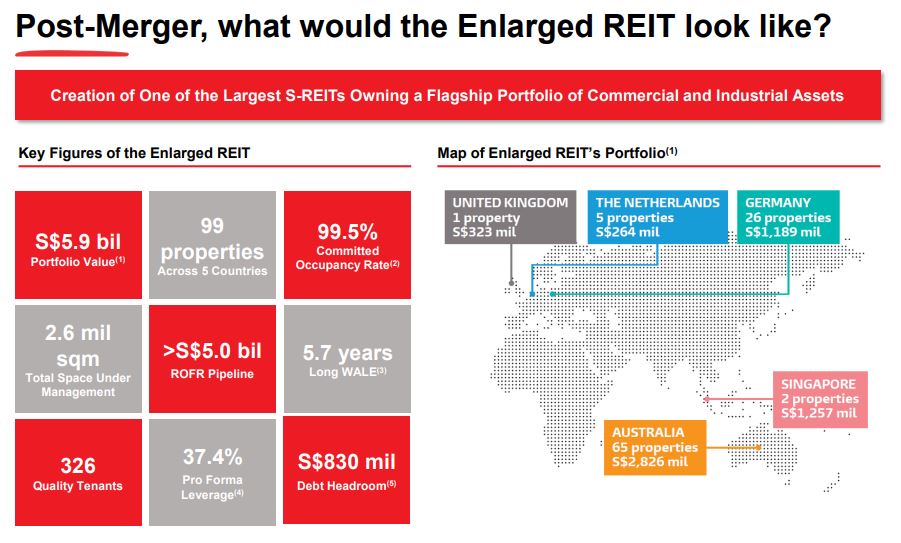

8. Frasers L&C Trust (SGX: BUOU)

Frasers Logistics & Commercial Trust is the combined entity after the merger between Frasers Logistics & Industrial Trust and Frasers Commercial Trust. It has a portfolio of 93 logistics and 6 commercial properties valued at S$5.9B diversified across 5 major developed markets - Australia, Germany, Singapore, United Kingdom and Netherlands.

93 Logistics Properties

1. Cross Street Exchange, a 15-storey commercial office in Singapore

2. Alexandra Technopark, a business park with 2 blocks of building and amenity hub in Singapore

3. Central Park, a 51-storey Grade A office building in Perth, Australia

4. Caroline Chisholm Centre, a 5-storey Grade A office in Canberra, Australia

5. 357 Collins Street, a 25-storey Grade A office building in Melbourne, Australia

6. Farnborough Business Park comprising 14 commercial buildings in London

I like the well-diversified portfolio of logistics, industrial properties and business parks in Australia and Europe, well decoupled from the Singapore economy. Most of the properties run on master lease with 100% occupancy, are freehold and have a long term lease with annual rent uplift. I am not keen of having 6 commercial properties in this Reit, but the top commercial tenant profiles of Australian government, Google and Rio Tinto excites me. The logistic tenant profiles are spread across various industries such as consumer, logistics services, manufacturing and automotives.

This Reit is solid, resilient and defensive because it is geographically diversified in high growth economies, has diverse high quality tenants from widespread industries and the huge number of properties reduce the default and tenancy risk. Its main downside is Forex risk from collecting revenue from various currencies. It is like an 'Ang Mo' version of Mapletree Logistics Trust which is rather Asian flavoured.

In terms of short and long-term growth prospects, it has a right of first refusal to a $5B portfolio of properties to choose from from its parent and sponsor, Frasers Property. At a current share price of $1.08, it yields 6.5% based on $0.070 dividend per share. There is definitely room and potential for their portfolio and share price to grow.

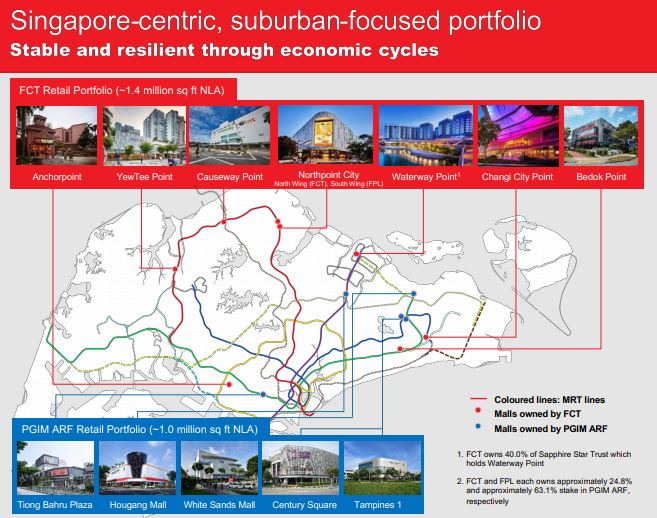

9. Frasers Centrepoint Trust (SGX: J69U)

Frasers Centrepoint Trust owns and invests in 7 suburban shopping malls in Singapore valued at $3.2B. All the retail properties are located on or beside MRT stations and bus interchanges. It is a pure play on Singapore domestic necessity retail spending, F&B and essential services. It also owns a 24.82% share in PGIM ARF which owns another 5 retail malls in Singapore and a 31.15% stake in Hektar Reit that owns 6 suburban shopping malls in Malaysia.

Since IPO in 2006, this Reit has delivered a consistent and steady increase in Net Property Income and DPU for shareholders until this current pandemic which may curtail the DPU for a few quarters in 2020. Occupancy is healthy at 97.3% as on 31 Dec 19 and rental reversion is positive at 5% for 1Q 2020.

Causeway Point, Northpoint City and Waterway Point are the three largest malls in the portfolio leveraging on the population growth potential of these HDB Towns. Key developments in the northern regions of Singapore such as Woodlands Regional Centre and Punggol Digital District, SIT's Punggol Campus, new Thomson-East Coast MRT Line serve as catalysts for this Reit to grow in the mid term future. As the supply of future suburban retail space is set to drop significantly in the future years, retail rentals should continue to grow steadily. Even though e-commerce penetration has affected the need for physical electronics and clothing stores, there is a chunk of tenants in Frasers shopping malls catering to tuition, childcare services, enrichment centres and gyms, which are essential services for nearby residents.

It is currently valuated at $2.08 with a yield of 5.2% based on estimated dividends of $0.11 per share. Fueled by population catchment growth, new MRT links, Singaporean' s liking of food and shopping, I certainly believe this Reit will propel again after the current situation is over.

10. Aims Apac Reit

It is the 5th largest industrial Reit behind the likes of Ascendas and Mapletree in terms of market capitalisation. It owns a $1.5B portfolio of 25 industrial properties in Singapore and 2 properties in Australia.

Australia properties

1. Optus Centre Business Park comprising six 4 and 5-storey buildings and a carpark in New South Wales, Australia

2. Boardriders APAC HQ, a warehouse, office and a retail showroom in Queensland, Australia

Singapore properties

A.Logistics and Warehouse

1. 8 and 10 Pandan Crescent

2. 10 Changi South Lane

3. 11 Changi South Street 3

4. 103 Defu Lane 10

5. 56 Serangoon North Avenue 4

6. 7 Clementi Loop

7. 3 Toh Tuck Link

8. 27 Penjuru Lane

9. 20 Gul Lane

10. 30 Tuas West Road

B. Light Industrial

11. 15 Tai Seng Drive

12. 23 Tai Seng Drive

13. 135 Joo Seng Road

14. 1 Kallang Way 2A

15. 1 Bukit Batok Street 22

C. General Industrial

16. 26 Tuas Avenue 7

17. 2 Ang Mo Kio Street 65

18. 61 Yishun Industrial Park A

19. 541 Yishun Industrial Park A

20. 8 Senoko South Road

21. 51 Marsiling Road

22. 8 Tuas Avenue 20

23. 3 Tuas Avenue 2 (Under Development)

D. Business Park

24. 1A International Business Park

E. Hi Tech

25. 29 Woodlands Industrial Park E1

This Reit rewards long-term shareholders with stable and sustainable DPU of above 10 cents per share every year even though there is limited growth in DPU and Net Property Income.

The occupancy in Singapore properties is 89.4% as at 31 Dec 2019, which is on par with JTC industrial average of 89.2%. The drop in occupancy is due to conversion from master leases to multi-tenancy leases at 1A International Business Park and 20 Gul Way. While rental reversions have been negative at 1.92% as of 31 Dec 2019, this Reit has undergone asset enhancement initiatives to unlock on its untapped gross floor area of its properties. Recent strategic moves have seen this Reit acquiring freehold property in Australia with long master tenant i.e the Board Rider APAC HQ and undergoing design-and-build redevelopment of 3 Tuas Avenue 2 into a versatile ramp-up industrial facility for a global medical device company who will be the master tenant for an initial 10 years lease.

Even with limited growth and absence of huge potential, I believe this is an undervalued and well managed small industrial Reit in relative to other midgets such as Cache which is renamed to ARA LOGOS, Sabana, ESR and Soilbuild Reit which are all in shit one way or another.

Besides providing stable returns, this Reit is a potential acquisition target for takeover by ESR and possibly other giants like Mapletree for reasons due to its fragmented shareholding structure and access to untapped gross floor area as mentioned by DBS Research.

Valuated at a market share price of $1.18, it yields an attractive 8.4% based on a conservative dividend of $0.099 per share. Since the branded industrial Reits are priced at a premium with squeezed yields, this unbranded industrial play still offers immense value, presents steady returns and a decent opportunity for an "en-bloc" windfall, it is a matter of time before this ugly duckling evolves to a swan.

Disclaimer: I am vested in 5 of the 10 Best Reits mentioned and my opinion may contain biasness. This sharing is not a Buy Recommendation for any of the Reits. Investment in Reits can result in huge capital losses. Do your own due diligence before any investment.

Anyway, thanks for reading.

With Love & Peace,

Qiongster

No comments:

Post a Comment