This is an update of my investment portfolios for Apr 2024.

My SGX Income Portfolio value rises to $366k from $347k due to capital injection for purchase of DBS and Reits.

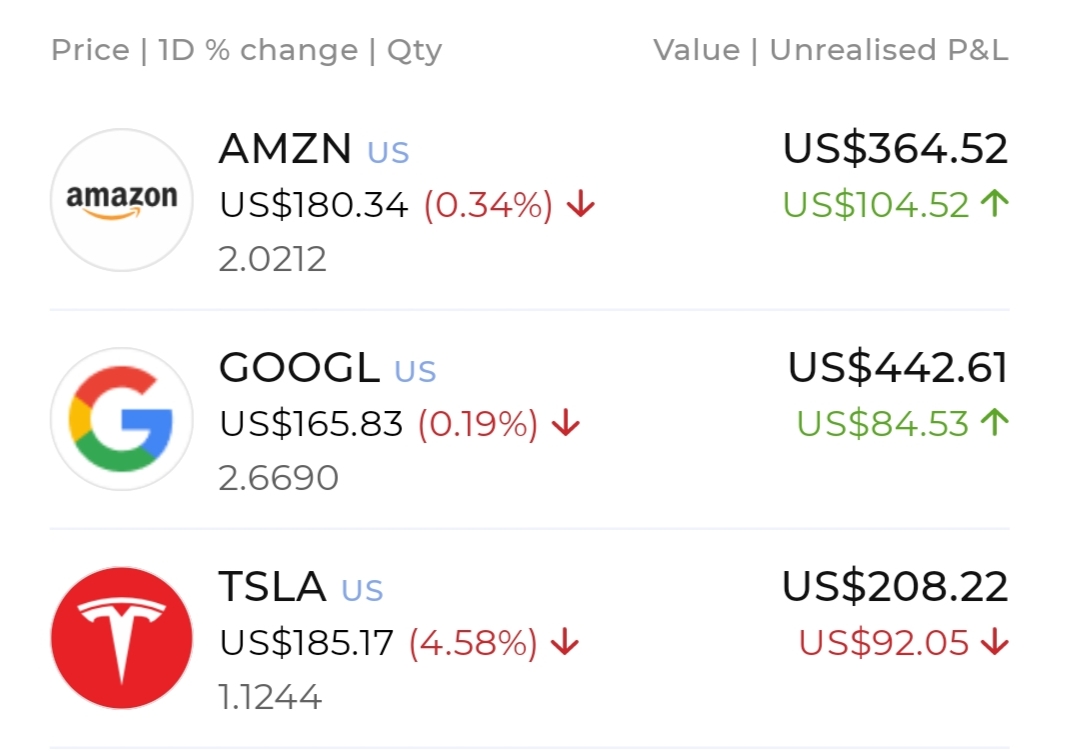

My US/HK Growth Portfolio value inches up to US$17.9k from US$17.7k.

My SRS Ultra Long-Term Portfolio value increases to $163k from $159k.

The US stock markets have attained fresh record highs amidst uncertainties over interest rates, ongoing wars and diminishing fears of global recession. US 10-year and 30-year government yields have rebounded and the Federal Reserve is expected to hold interest rates high with a possibility of no rate cut for the year.

Despite being clouded by uncertainties, immense noises and fears, it is crucial that long-term investors like us always remain calm, unwavered and focused on our investment objectives. Stick to our own plan and continue deploying our financial resources into high quality income-producing instruments such as government-backed risk-free bonds, property assets, or strong growth businesses tactfully according to our own risk appetite.

This is a month when I am planting more seeds for the future.

Portfolio Actions

Portfolio Dividends

1. Received $302.17 of dividends from Savings Bonds on 1 Apr.

2. Received $340 of dividends from Frasers Centrepoint Trust on 2 Apr.

3. Received $324 of dividends from DBS on 19 Apr.

4. Received 91 bonus shares from DBS on 30 Apr.

SGX Income Portfolio

Portfolio Value = $366k

Moomoo

Tiger Broker

Syfe Trade

SRS Ultra Long-Term Portfolio